The move aims to generate revenue that would help cover the costs of continuous development and digital transformation initiatives undertaken by banks.

Finance (Category)

Showing all articles in this category.

Browse Our Latest Articles

March 12, 2025

Kuwait: Banks Consider Imposing Fees on Online Transfers

December 3, 2024

Cash Crunch Pushes Libyans to Bank Cards Despite Hurdles

In Libya, a shortage of cash in the banking system has pushed many to turn to cards for payments.

August 29, 2024

Holiday Scam Warning for South Africa: How to Protect Yourself From Increasing Banking Fraud

The end of the year is fast approaching, and with it, the festive season and general anticipation for that hard-earned vacation that many South Africans work so hard for during the year. While this is a time of good cheer and increased shopping a...

August 22, 2024

Transforming Global Finance: The Impact of Continuous Transaction Controls on Tax Compliance

While the global economy is becoming increasingly interconnected, the need for standardized financial processes has never been greater. Continuous Transaction Controls offer a relatively new approach to transaction data reporting and verification ...

July 31, 2024

How Nigerian Investors Can Tap into UK Social Housing with Yield Investing

In recent years, savvy Nigerian investors have been expanding their portfolios beyond local markets, seeking stable, high-yield opportunities abroad.

July 25, 2024

How Data Sharing Can Drive Financial Inclusion in Africa

Despite the access to financial services that mobile money has introduced across Africa, a significant portion of the population remains unbanked and underserved. Data sharing holds the key to unlock the continent's vast economic potential. ...

June 28, 2024

Why the Promise of a Cashless Society is Key to Unlocking the Nigerian Commerce Growth Opportunity

Cash is a uniquely expensive and inconvenient way to do business. However, shifting to a world of cashless payments is easier said than done, as many policymakers have discovered to their cost. The Nigerian Government is taking unprecedented steps...

May 14, 2024

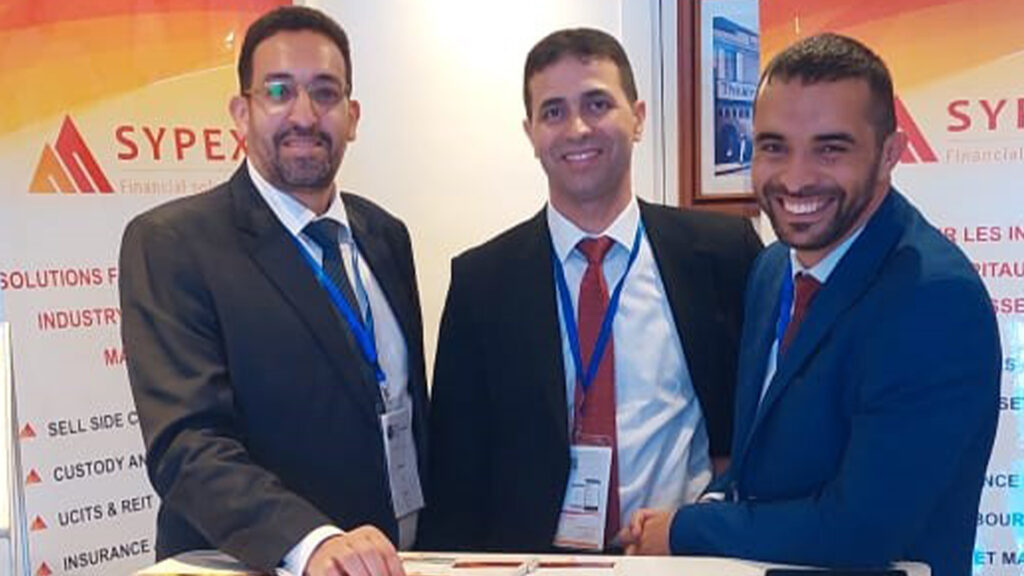

Best Capital Market Fintech Company – EMEA

Delivering unparalleled fintech solutions for capital market industries, SYPEX introduces its software to a plethora of clients withing to invest, and manage their investments, with ease. Here we learn more from Co-founder and Associate Director H...

April 23, 2024

China Writes Off Interest-Free Loans Given To Zimbabwe

China has written off an unspecified amount of Zimbabwe's interest-free loans and pledged to help the Southern African country find a way out of its debt crisis, even as activists warned of a permanent debt trap.

April 23, 2024

Food Inflation Dip Drives Headline Figure Lower in SA

After a brief upward trend spanning two months, the headline inflation rate in South Africa showed signs of moderation, declining from 5.6% in February to 5.3% in March.

April 9, 2024

AI Central to Nigeria’s Insurance Future – Stakeholders

The regulatory body for insurance in Nigeria has acknowledged Artificial Intelligence (AI) as being key to the future of insurance business in the country.

March 26, 2024

February Salary Surge Indicates Positive Trend for Yearly Pay Increases in SA

The monthly BankservAfrica Take-home Pay Index (BTPI) experienced another positive month in February amid the better-performing environment, resulting in companies increasing their employees' average salaries over the last three months.

Looking for a particular article?

Learn More About MEA Markets

Product Brochure

Product Brochure

Our product brochure contains a comprehensive overview of the branding and recognition opportunities we offer. It features a range of magazine front cover and editorial examples, as well as newsletter examples, a selection of our prestigious trophies and plaques, and a variety of digital offerings designed to enhance visibility and impact.

Media Pack

Media Pack

Our media pack contains everything you need to understand our brand’s reach and opportunities. It offers a detailed look at our awards programmes, advertising options, testimonials, upcoming features, and more, making it an essential resource for businesses looking to maximise their visibility across the Middle East and Africa.

Trusted by the best teams around the world